Oil just dropped -28% and -24% respectively in back to back months with intervening rallies back up to $35. The spot oil market is turning into a no bid market and therefore a no-brainer short of the front month contract and a risk-free arbitrage of the ETF relative to the next month contract...

"We ain't seen nothin' yet"

When the Spot/1-Month spread gets as wide as 2009, the price drops will be 2x what we've seen so far, just to find "the market". Last month saw an $11 nine-month spread to bring in arbitrage buyers, and form a temporary low. At the 2009 bottom, the 12 month "super contango" spread was $22, which implies $18 spot price from these levels. And long-dated futures are still highly correlated to near-term futures, making the "bottom" a moving lower target...

Once a month, the oil futures market visits the spot oil market for a reality check. The rest of the time, the bullshit flows hot and heavy as the futures market is manipulated ten ways to Sunday via the daily OPEC deal, short-covering, 20x leverage, and CNBS 24x7...

Oil ETF short positions surged 300% in one month

This is the current front-month contract aka. quoted price of oil. As we see, once per month, the futures figure out that the spot market is well below the futures market, and going lower every month...

Traders are starting to front-run expiration (4th business day before 25th of month), by pounding the expiring contract earlier each month to "find the market". Regardless of where oil is trading ahead of time, the last two "rollovers" saw a -10% drop in oil in the two days prior to ditching the expiring contract. The nine month contango spread was $11 in February and $8 in January...

Here is the 2009 bottom:

As we see it can take a few -30% "visits" to the basement before the market finds bottom.

Risk free arbitrage visualized

Long next month contract, short ETF (expiring contract):

The ETF absorbs the entire spread every single month...it's an arbitrage profit. As long as the glut persists, this short trade will make money...

Because, this sets the true price of oil:

Oil inventories:

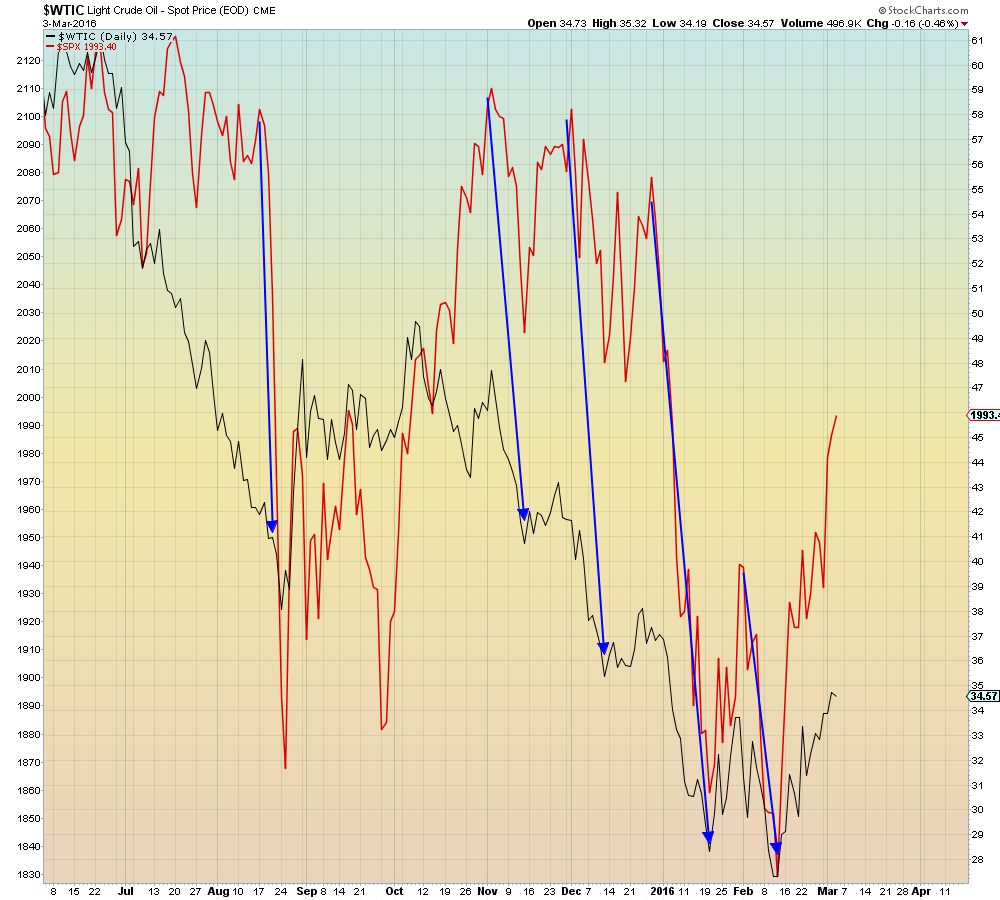

S&P 500 with oil: