Two years ago this month, Zerohedge wrote, "This Is What Happens If Volatility Goes Bananas". The author predicted the volatility short trade would implode overnight. And it literally did only a few months later, during VolPlosion 1.0. But of course, it did not end the volatility short trade by any means. Volatility gamblers were taught another good lesson in the fourth quarter, but they didn't learn from that one either. They have become systematically desensitized to ever-greater risk...

Despite the sea of tranquility at all time highs, the Wall Street Journal has noticed a "gamma trap" door lurking below the new "permanent plateau":

CNBC Discussed this phenomenon here as well:

To paraphrase, large institutions - having traded out of stocks and back into fixed income - have decided to leverage their returns by selling put options below the market. Basically saying, "We don't like stocks at this level, but we would own them lower. In the meantime, we will collect fat option premium". All well and good, however, this tsunami of put selling has artificially levitated the casino, as market makers are forced to hedge the other side of the position by buying stock. This large scale "dynamic hedging" has served to massively increase sensitivity (gamma) to underlying market moves. Now reaching an extreme level, despite or because of the sea of tranquility. Meaning their collective actions have artificially collapsed volatility while amplifying sensitivity to volatility. But what could go wrong?

As expected, this systemic risk amplifying strategy is now being marketed as a risk-reducing strategy. In other words, a way to increase commissions when institutions are largely "RISK OFF".

Rewind to the May sell-off:

"The options-selling strategy, now a multi-billion dollar juggernaut, was one way Wall Street warded off steep losses this month."

Real money and hedge funds have heeded Wall Street advice to systematically sell insurance against price swings as a way of getting exposure to the bull market."

While estimates are hard to come by, the amount of institutional put-selling is anecdotally vast enough to push down implied volatility in U.S. stocks, potentially creating an illusion of market serenity. And should stocks drop dramatically, dealer hedging may exacerbate losses, a phenomenon dubbed a gamma trap.

Under the banner of "what could go wrong", tomorrow Powell addresses the House, and FOMC minutes are released in the afternoon.

Here are a few more things to consider:

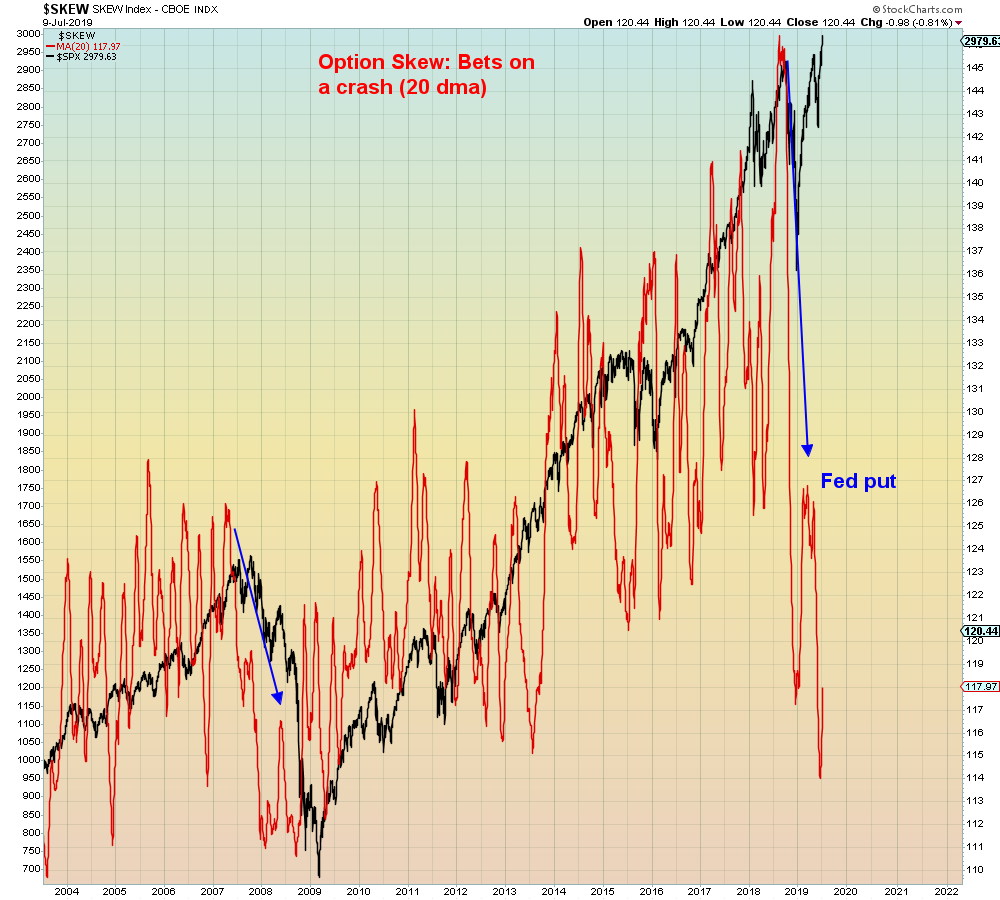

In summary, there is no such thing as a "Fed put". Yet another Wall Street imagined reality at client expense...