Yesterday, Senate majority leader, Mitch McConnell, stated that tax reform is highly unlikely in FY17 (end of September). Small cap stocks, the primary beneficiary, were hammered on the week.

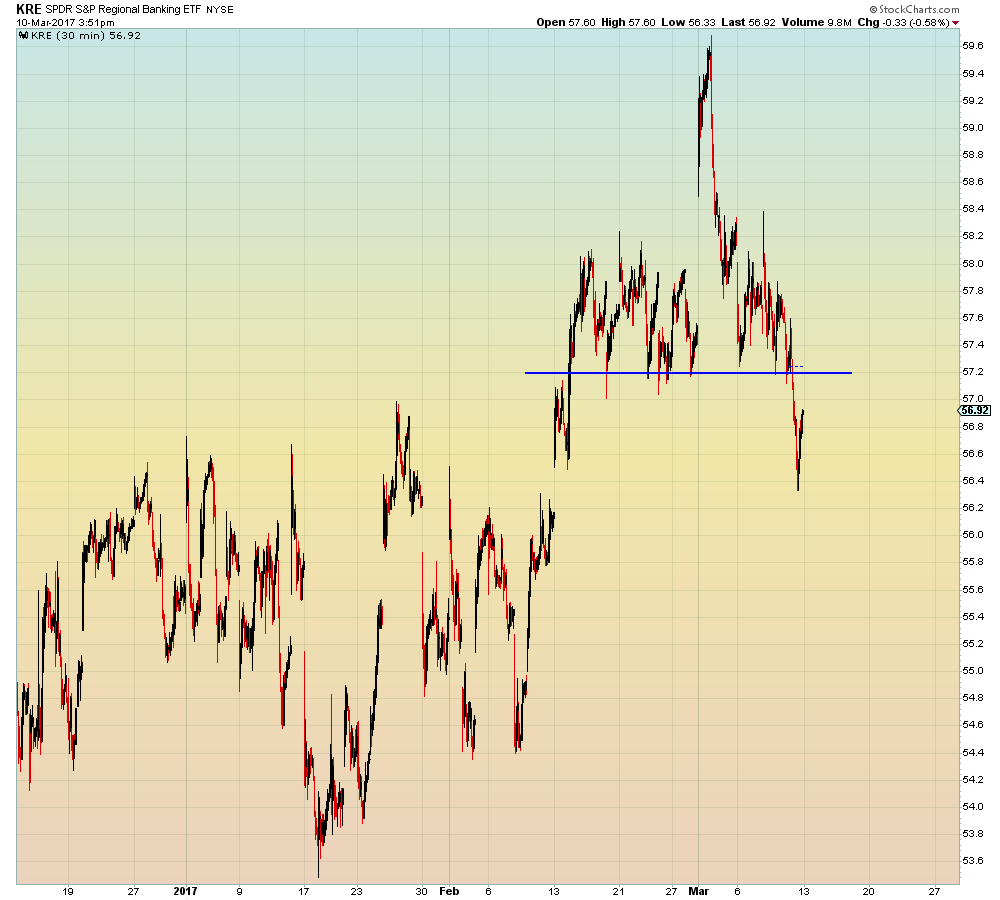

Yesterday, White House spokesperson, Sean Spicer, confirmed that Trump is still intent on bringing Glass-Steagall back. Bank stocks hammered on the week.

Also yesterday, OPEC signaled that extension of the January output cut past May is highly unlikely due to the resurgence of U.S.-based shale oil. Oil down -9% on the week.

Today, Secretary of the Treasury, Mnuchin, signaled ahead of next week's G20 meeting that the new administration won't tolerate competitive currency devaluation. That is imploding the inbound dollar carry trade aka. USDJPY.

Next week, the implosion fest will be accelerated by the third Fed rate hike and the fiscal cliff clusterfuck 2.0, which will final implode the 'infrastructure stimulus' trade.

The chart of the week has to be this one of regional banks:

Short-term view:

Oil with C$:

$USD ETF

Junk bonds