Social Mood was delayed but not denied...

Monetary Policy Is The Decoupling of The Economy From Financial Markets. Globalization Is The Decoupling of Supply From Demand. Combined, They Led To Human History’s Largest Misallocation of Capital

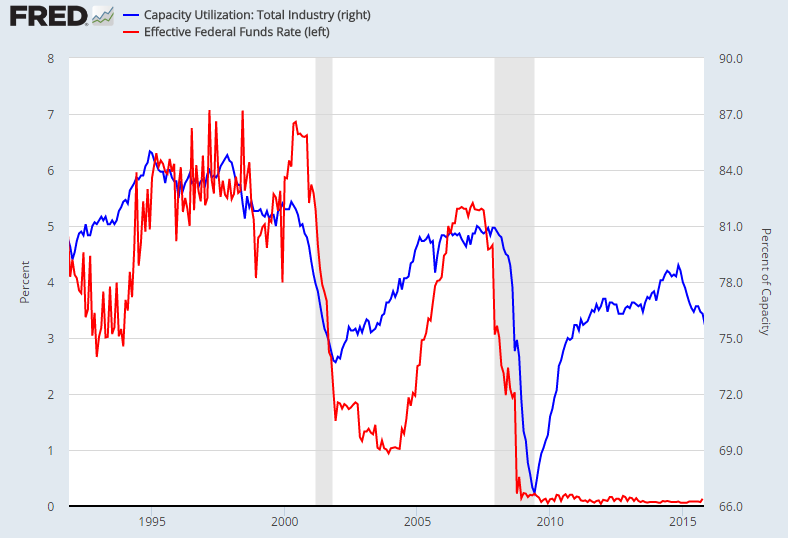

The Globalized era proved that economists don’t understand financial markets and financial gurus don’t understand the economy. And neither party tracks both. In an unmanaged economy, financial markets invest at the prevailing cost of capital based upon an expected future return on investment. The future is always uncertain, which assures that capital is closely rationed to ensure maximization of future profit and minimization of future loss. Monetary policy however, is the manipulation of the cost of capital to incentivize investment without regard to future return. Economists merely take it as a leap of faith that the economy will always improve over the course of the “cycle” and hence their subsidization of capital will be rewarded in the future. Unfortunately, Globalization disrupted that historically valid assumption due to the ever-growing supply/demand imbalance. Investments in supply at the beginning of the cycle resulted in overcapacity at the later stages of the cycle, which is the exact opposite of historical precedent. Capital markets were making their same historically-rewarded cyclical growth assumption without regard to the fact that cyclical growth on a debt adjusted basis was not actually occurring. The media diligently reported that on an industry by industry basis there was oversupply in oil, retail, commodities, real estate, shipping, automobiles - everything. However, they never connected the dots that oversupply was rampant across all industries and hence capital was massively misallocated at the end of the cycle:

Capacity Utilization with Fed Rate

Earnings yields normally rise throughout the cycle as investments come to fruition. Here we see in this cycle Corporate profits tracked global growth lower. This was all explained away, but it was really a function of 0% interest rates and a dearth of investment alternatives due to lack of demand.

The inexorable global deflationary pull of interest rates towards the zero bound, assured that the historical “rotation to cash” which occurs at the end of the cycle, would never happen. Instead, investors fled to the perceived “safety” of over-crowded high yielding assets.

Rotation to yield was misconstrued as rotation to safety...

Cash balances with dividend yield fund

U.S. Deflation (black) with global yields

Nevertheless, Central Banks facilitated excessive speculation at the end of the risk cycle.

Here we see that the cyclically played out IPO market exhibits an additional late stage rally that was not evident at the end of the 2008 cycle, due to post-Brexit stimulus:

Likewise the Canadian market rallied into a GDP decline: